As detailed below, the potential returns are:

1. Delta Air Lines Inc.: +0.9% absolute return in 17 days (equivalent to a +19.8% annualized return-on-investment)

2. General Motors Inc.: +1.8% absolute return in 17 days (equivalent to a +37.9% annualized return-on-investment)

Note: the Implied Volatility (IV) of the options at the time they were sold was 37 for Delta and 24 for GM, so each option exceeded the Covered Calls Advisor's minimum threshold of IV>20 and thus provides a sufficiently attractive potential return-on-investment relative to the conservative risk profile of each position.

1. Delta Air Lines Inc. (DAL) -- New 100% Cash-Secured Puts Position

The transaction was as follows:

03/02/2016 Sold 3 DAL Mar2016 $45.00 100% cash-secured Put options @ $.45

Note: the price of DAL was $47.83 today when this transaction was executed.

The Covered Calls Advisor does not use margin, so the detailed information on this position and a potential result shown below reflect the fact that this position was established using 100% cash securitization for the Put options sold.

A possible overall performance result (including commissions) would be as follows:

100% Cash-Secured Cost Basis: $13,500.00

= $45.00*300

Note: the price of DAL was $47.83 when these options were sold

Net Profit:

(a) Options Income: +$124.80

= ($.45*300 shares) - $10.20 commissions

(b) Dividend Income: +$0.00

(c) Capital Appreciation (If DAL is above $45.00 strike price at Mar2016 expiration): +$0.00

= ($45.00-$45.00)*300 shares

Total Net Profit (If DAL is above $45.00 strike price at Mar2016 options expiration): +$124.80

= (+$124.80 options income +$0.00 dividend income +$0.00 capital appreciation)

Absolute Return (If DAL is above $45.00 strike price at Mar2016 options expiration): +0.9%

= +$124.80/$13,500.00

Annualized Return: +19.8%

= (+$124.80/$13,500.00)*(365/17 days)

The downside 'breakeven price' at expiration is at $44.55 ($45.00 - $.45), which is 6.9% below the current market price of $47.83.

Using the Black-Scholes Options Pricing Model in the Schwab Hypothetical Options Pricing Calculator, the probability of making a profit (if held until the Mar 18th, 2016 options expiration) for this DAL short Puts position is 79%. This compares with a probability of profit of 50.3% for a buy-and-hold of DAL shares over the same time period. Using this probability of profit of 79%, the expected value annualized return-on-investment (if held until expiration) is +15.6% (+19.8% * 79%), an attractive risk/reward profile for this conservative investment.

The 'crossover price' at expiration is $48.28 ($47.83 + $.45). This is the price above which it would have been more profitable to simply buy-and-hold DAL until the Mar2016 options expiration date rather than selling these Put options.

2. General Motors Corporation (GM) -- New Covered Calls Position

An ex-dividend occurs on March 9th of $.38. Although somewhat unlikely, if the

current time value (i.e. extrinsic value) of $.21 [$1.17 option premium -

($29.96 stock price - $29.00 strike price)] remaining in the short call

options decay further by March 8th (the business day prior to the ex-dividend date), there is

a possibility that the Call options owner would exercise early and

therefore call the 300 GM shares away to capture the dividend payment.

An ex-dividend occurs on March 9th of $.38. Although somewhat unlikely, if the

current time value (i.e. extrinsic value) of $.21 [$1.17 option premium -

($29.96 stock price - $29.00 strike price)] remaining in the short call

options decay further by March 8th (the business day prior to the ex-dividend date), there is

a possibility that the Call options owner would exercise early and

therefore call the 300 GM shares away to capture the dividend payment. As shown below, two potential return-on-investment results for this position are:

If Early

Assignment: +0.5% absolute return (equivalent to +26.0% annualized

return for the next 7 days) if the stock is assigned early (business

day prior to Mar 9th ex date); OR

If Dividend Capture: +1.8%

absolute return (equivalent to +37.9% annualized return over the next 17

days) if the stock is assigned at the Mar2016 expiration on March

18th. The transactions were:

03/02/2016 Bought 300 GM shares @ $29.96

03/02/2016 Sold 3 GM Mar2016 $29.00 Call options @ $1.17

Note: a simultaneous buy/write transaction was executed.

03/09/2016 Upcoming ex-dividend of $.38 per share

Two possible overall performance results (including commissions) for this GM covered calls position are as follows:

Stock Purchase Cost: $8,995.95

= ($29.96*300+$7.95 commission)

Net Profit:

(a) Options Income: +$340.80

= ($1.17*300 shares) - $10.20 commissions

(b) Dividend Income (If option exercised early on business day prior to Mar 9th ex-div date): +$0.00; or

(b) Dividend Income (If GM assigned at Mar2016 expiration): +$114.00

= ($.38 dividend per share x 300 shares)

(c) Capital Appreciation (If GM assigned early on Mar 8th): -$295.95

+($29.00-$29.96)*300 - $7.95 commissions; or

(c) Capital Appreciation (If GM assigned at $29.00 at Mar2016 expiration): -$295.95

+($29.00-$29.96)*300 - $7.95 commissions

+($29.00-$29.96)*300 - $7.95 commissions; or

(c) Capital Appreciation (If GM assigned at $29.00 at Mar2016 expiration): -$295.95

+($29.00-$29.96)*300 - $7.95 commissions

Total Net Profit (If option exercised on day prior to Mar 9th ex-dividend date): +$44.85

= (+$340.80 +$0.00 -$295.95); or

Total Net Profit (If GM assigned at $29.00 at Mar2016 expiration): +$158.85

= (+$340.80 +$114.00 -$295.95)

1. Absolute Return [If option exercised on Mar 8th (business day prior to ex-dividend date)]: +0.5%

= +$44.85/$8,995.95

Annualized Return (If option exercised early): +26.0%

= (+$44.85/$8,995.95)*(365/7 days); OR

2. Absolute Return (If GM assigned at $29.00 at Mar2016 expiration): +1.8%

= +$158.85/$8,995.95

Annualized Return: +37.9%

= (+$158.85/$8,995.95)*(365/17 days)

In this instance, early assignment provides a lower annualized return, so capturing the dividend and being assigned at Mar2016 expiration is preferable; but either outcome would provide an attractive return-on-investment result for this investment. These returns will be achieved as long as the stock is above the $29.00 strike price at assignment. If the stock declines below the strike price, the breakeven price of $28.79 ($29.96 -$1.17) provides 3.9% downside protection below today's purchase price.

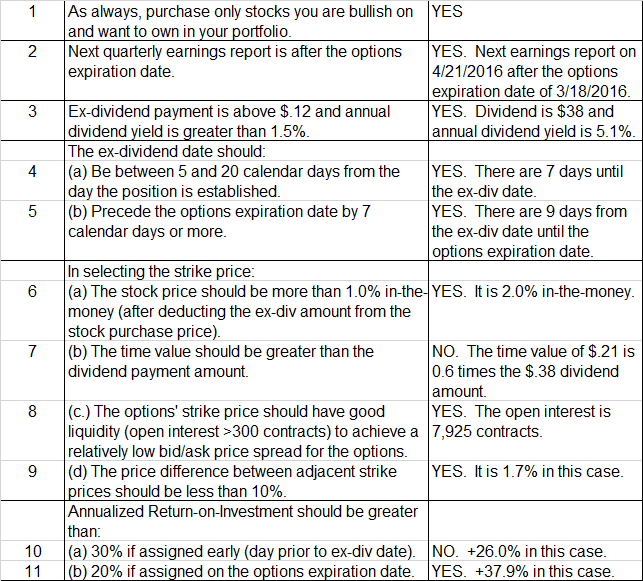

The Covered Calls Advisor has established a set of eleven criteria to evaluate potential covered calls using a dividend capture strategy. The minimum threshold to establish a position is that at least nine of these eleven criteria must be achieved, which for this GM position was the case (as shown in the table below).